Fiat currency is dying a natural death — its logical replacement is a digital voucher system fixed to labour time

British pound sterling has devalued by more than 99.5% since the year it was founded (1694). The US dollar, the global reserve currency, has lost 96% of its purchasing power since 1913, having barely lost any before then. The figure is 91% when the starting point is taken from 1947, when the US became the world’s leading imperialist power; and 85% since 1970. That means today’s dollar was worth nine cents in 1949 and 15 cents in 1970. The dollar’s rate of inflation has been 3.92% per year since 1970, compared to 0.46% per year before then. Even the Chinese renminbi in 2019 was worth only 22% of its 1987 equivalent.

China, the main financer of US national debt, has been diversifying its foreign reserves, along with Russia and even Saudi Arabia. In the first quarter of 2020, the dollar’s share of trade between Russia and China fell below 50% for the first time on record. As recently as 2015, approximately 90% of the transactions were conducted in dollars. At the same time, the euro made up an all-time high of 30 per cent, while their national currencies accounted for 24 per cent, also a new high. Even JP Morgan, the US’s biggest bank, told its clients in August 2019 to sell the dollar.

Capital is becoming increasingly dependent on the state to sustian the ever-greater demands of accumulation. As of 29 February 2020, the Fed held $2.47 trillion, 14.6%, of $16.9 trillion marketable US Treasury securities outstanding, making it by far the largest single holder of US Treasuries in the world. By the end of March, this increased by an unprecedented monthly increase of $650bn, to $3.12 trillion. One estimate said that if this pace of buying continued, the Fed would “own the entire Treasury market in about 22 months”. As of 23 November, 21% of all US dollars had been printed in 2020, taking the figure to 75% over the past 12 years — already sparking fears about possible hyperinflation.

All this is happening because the historical (ie inevitable) rise of automated production is abolishing the source of exchange-value creation — capital’s exploitation of commodity-producing human labour.

Human labour is the source of exchange-value, but under capitalism this value is only realised through commodity sales. The true measure of exchange-value is labour time. So the quicker it takes to make something (and transport to its place of sale), the cheaper it becomes to buy. Hence the exponential decrease over the past 40 years in computing and other consumer prices. 3-D printing is especially accelerating the trend of prices falling to zero.

For example, whereas the world’s fastest supercomputer in 1975 was worth $5m ($32m in 2013’s money), the price of an iPhone 4 released in 2010 with the equivalent performance was $400. Aerospace companies producing propulsion systems in 2010 for $24m in 24 months are now 3-D printing their engines for $2,000 in two weeks.

This is further reflected in the falling general rate of profit, which is falling historically towards zero.

Automation is inevitable not just in terms of historical progress but because the ever-rising demands of capital accumulation demands ever-higher productivity. The capitalist system is therefore all but abolishing itself.

Indeed, with interest rates already at zero, capitalism is soon likely to spiral into a crisis of worldwide hyperinflation. Banks hit out at the prospect, saying it would slash their earnings and limit their ability to absorb loan losses. Bank of America analysts estimated that a BoE rate cut of just minus-0.25% would depress the banking sector’s average return on equity into low-to-mid single digits and take 50% off Barclays’ domestic pre-tax profit, rising to more than 70% for RBS and Virgin Money.

Ultimately, negative rates would at some point deliver the final devaluation of currency. But lifting an economy out of recession has take (on average since 1958) a 6% base rate cut, and so far since February 2020 they have only been cut by around 1–2%. Some, in Europe in Japan, were already negative. Central banks are stuck between a rock and a hard place.

The threat of worldwide hyperinflation therefore looms and fits historically and logically with the devaluation of the past 100 years. Worldwide hyperinflation would see the worth of all fiat currencies collapse against precious metals.

Financial economist Jim Rickards predicts that if gold became the world currency standard, its price would rise by 700% from $1,400 per ounce (as of August 2019, having risen from about $250 in 2000) to $10,000 per ounce, presumably leaving the vast majority of people potentially seven times poorer.

During the first quarter of 2019 — in anticipation of what lies ahead — central banks bought 145.5 metric tonnes of gold, compared to 86.7 metric tonnes in the first quarter of 2018, a 68% spike, according to the World Gold Council. The overall figure in 2018 was 651.5 metric tonnes, up by 74% from 2017 and the second highest yearly total on record.

The labour theory of value

Rickards, a right-wing libertarian, believes in the subjective theory of value — that something is worth what someone is willing to pay for it (this despite recognising that GDP growth depends on the size and productivity of labour!). Rickards mocks Marx for asserting that gold has no intrinsic value. But Marx is right. Like any other commodity, gold’s value depends on how long it takes labour to produce it. Once capitalism bottoms out, gold will be as worthless as fiat money, at least to most people. Gold production too is being automated. Indeed, even Rickards has admitted that the next crisis will “discredit capitalism for good”.

That commodity-producing human labour is the source of exchange-value creation and profit is obscured by the commodity/money-form (gold is the money-commodity). As mentioned, value is really measured in time. The worker sells her labour power (the ability to work) to the capitalist but only takes home what she needs to live on (necessary labour time) — say, for example, four hours out of eight per day — and the capitalist keeps the rest (surplus labour time/surplus value), which is realised through the sale of commodities.

But because capitalism only produces when it is profitable to do so, it suffers from periodic economic crises, which result from an inevitable underproduction of surplus value relative to total capital. To revive growth, the capitalist has to raise the rate of exploitation. Innovation results in necessary labour time falling and surplus labour time rising, say, as per our example, to three and five hours respectively. But fewer exploitable workers are employed relative to the expanded total capital, and in the long run (recessions tend to strike on average every 10 years), the underproduction of surplus value reasserts itself, and to a greater extent.

With humans increasingly removed from the production process by automation, capitalism is heading ever-closer to its final crisis. As McKinsey Global Institute director James Manyika said in June 2017, “Find a factory anywhere in the world built in the past five years — not many people work there.”

The socialist necessity

In contrast, socialism (aka the ‘lower stage’ of communism), produces according to utility, to what’s deemed useful. Social ownership enables production to happen on a break-even basis, abolishing recession; and also enables actual full, formal employment, since it becomes possible for all labour — employed by society, via state enterprises — to become productive of value, ie of use-value (utility/usefulness), rather than profit/surplus value/exploitability. That means ending the chronic understaffing that characterises capitalism in areas such as teaching and nursing, since the labour time of teachers and nurses would contribute to economic growth instead of being paid out of the surplus value created by commodity-producers.

The required change in the mode of production then, in theory, is simple: nationalise/socialise the means of production, replace for-profit commodity-production with break-even utility-production and peg the ‘currency’ value to labour time. This would begin to and progressively enable us to fix society’s problems, without the ruinous disruptions of unemployment and recession, since society tends to become meaner when relative scarcity rises (as we have seen with the past 10 years of austerity), and vice-versa.

Non-transferable labour credits

In Critique of the Gotha Programme, Marx explains that under socialism workers would be paid in vouchers or certificates and then draw down entitlements (use them to purchase and consume goods). Such vouchers, or labour credits, would be non-transferable, cancelled once spent, like train tickets. So while socialism would incentivise and reward work, it would also prevent most wealth from accumulating in the hands of a few. Economic exploitation would be abolished and labour power decommodified. Exchange-value still exists but it is qualitatively different, now based on use-value instead of surplus-value.

With Britain’s cash economy already “close to collapse”, according to the Access to Cash Review, it is therefore time to transition to a digital voucher/credit system. Six and a half hours of work will be rewarded with 6.5 labour credits, enough to buy goods that collectively took six and a half hours to produce, and so on.

In Towards A New Socialism, Paul Cockshott and Allin Cottrell argue convincingly for the system described above, but with a grading system to incentivise the type of work and productivity rates.

This system also makes budgeting far more intelligible, enabling a much more informed electorate, who could vote on how much should be spent on each area of state spending. Cockshott and Cottrell argue for a flat rate tax (say 40% of every 1.0 labour credit, for argument’s sake) to fund state expenditure on health care, education, infrastructure investments, and so on.

Consumer goods prices would also be adjusted by a marketing algorithm according to supply and demand (and shrinking labour content, given the ongoing transition to full automation) to ensure stability (the price of a product rises against excess demand while the planners order its increased production; and vice-versa).

Cockshott explains:

“Suppose a radio requires 10 hours of labor. It will then be marked with a labor value of 10 hours, but if an excess demand emerges, the price will be raised so as to eliminate the excess demand. Suppose this price happens to be 12 labor tokens. The radio then has a price to labor-value ratio of 1.2. Planners (or their computers) record this ratio for each consumer good. The ratio will vary from product to product, sometimes around 1.0, sometimes above (if the product is in strong demand), and sometimes below (if the product is relatively unpopular). The planners then follow this rule: Increase the target output of goods with a ratio in excess of 1.0, and reduce it for those with a ratio less than 1.0.

“The point is that these ratios provide a measure of the effectiveness of social labor in meeting consumers’ needs (production of `use-value,’ in Marx’s terminology) across the different industries. If a product has a ratio of market-clearing price to labor-value above 1.0, this indicates that people are willing to spend more labor tokens on the item (i.e. work more hours to acquire it) than the labor time required to produce it. But this in turn indicates that the labor devoted to producing this product is of above-average `social effectiveness.’ Conversely, if the market-clearing price falls below the labor-value, that tells us that consumers do not `value’ the product at its full value: labor devoted to this good is of below-average effectiveness. Parity, or a ratio of 1.0, is an equilibrium condition: in this case consumers ‘value’ the product, in terms of their own labor time, at just what it costs society to produce it. This means that the objective of socialist retail markets should be to run at break even level, making neither a profit nor a loss; the goods being sold off cheap compensate for those sold at a premium.”

A central marketing authority would regulate the standards of consumer goods, with enterprises motivated to make attractive products by the raised market prices. The progressive increase in free time for workers as production becomes more efficient will act as an incentive to both work and improve efficiency. In the long run, Marx anticipates free time becoming the measure of social wealth, with more and more free time increasingly unleashing human creativity and reviving independent craftsmanship.

Revolutionary pedagogy

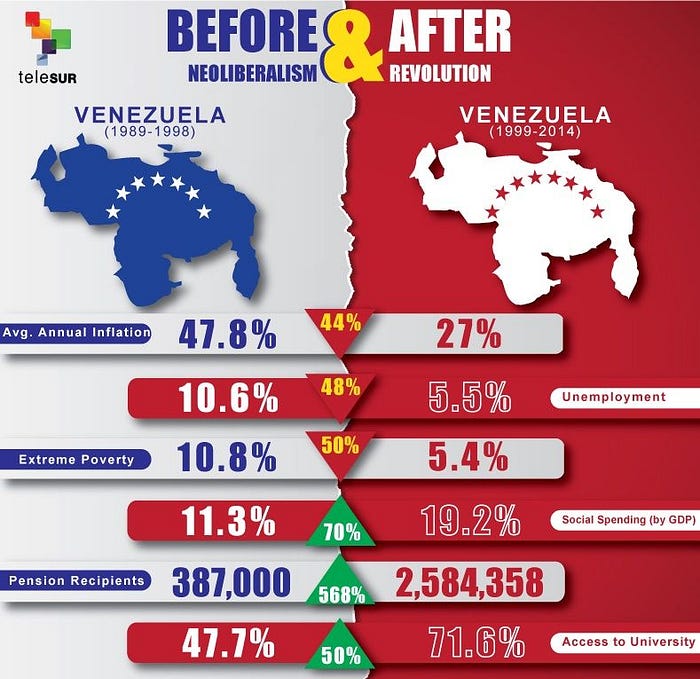

Even under capitalism, fixing currency to labour is one of the most important reforms socialists and workers should pursue. In Arguments for Socialism, Cockshott argues for such a reform in Venezuela, where the democratic socialist PSUV government has brought about a de facto situation of dual power (around 70% of the economy remains privately owned and so the economy remains capitalist, though many gains have been made that all socialists should support). He argues that the PSUV government should fix the value of the Bolivar to labour, rather than the cost of living, for two reasons (p161):

- As labour productivity rises, a Bolivar fixed in terms of hours of labour will be able to buy more each year, cheapening the cost of living.

- Once the value of the Bolivar has stabilised in terms of value of labour then the labour value of Bolivar notes should be printed on them in hours and minutes. This step would be an act of revolutionary pedagogy. It would reveal clearly to the oppressed just how the existing system cheats them. Suppose a worker puts in a working week of 45 hours and gets back Bolivars and sees that the hours printed on them only amount to 15 hours. Then she will become aware that she is being cheated out of 30 hours each week. This will act to raise the socialist consciousness of the people, and create favourable public opinion for other socialist measures.

Pegging currency to labour time would then have something of a They Live sunglasses effect.

Cockshott then advocates for an accounting reform (p162):

“All firms have currently to prepare money accounts. The government should make it a condition of their accounts being approved for auditing that they also produce labour time accounts, and that they mark all products with their labour content. Initially firms need not be legally obligated to sell their commodities at their true values. They could attempt to sell them for a price that is higher or lower than the true value. But since the consumer can now see when they are being overcharged, consumers will tend to avoid companies that sell goods at above their true value. This will put psychological and consumer pressure on companies that are overcharging. This, too, will be an act of socialist mass pedogogy, raising consciousness.

“In the first few months before all goods have their labour values printed on their price tags, firms will have to impute labour values to the goods they purchase using the printed exchange rate between Bolivars and labour hours. They will add to the labour value of their inputs, the number of hours of work that are performed by their employees to get a labour value for the final product.

“The government should also move towards having a dual system of national accounts, labour accounts alongside money accounts because at the level of national economic policy there are many issues on which labour accounts would be more informative than money accounts. Money accounts hide the fact that what government economic policy really does is reallocate society’s labour.”

Cockshott also rightly says that recognition of Marx’s labour theory of value, which has been proven by statistical mechanics, should be incorporated in law (pp162–3).

“The law should recognise that labour is the sole source of value and that in consequence workers, or their unions, will have a claim in law against their employers if they are paid less than the full value of their labour.

“If we consider the previous measures and the revolutionary pedagogy that would follow from them it should be relatively easy to pass a referendum on such a law. Following such a law being passed, there would be a huge wave of worker activism as workers and unions sought to end the cheating and to see which day and their ancestors had been subjected. It would also bring about a very large increase in real wages, cementing support for the socialist government. The employing class on the other hand would see sharp falls in their unearned incomes. Employers who were active factory managers would of course still be legally entitled to be paid for the hours that they put in managing the firm, just like any other employee.”

In summary, pegging currency to labour should be at the top of the list of socialist and working class demands, but in historical terms, it is now also — for the first time given the senility of capitalism and the advanced development of the productive forces — becoming an economic necessity, along with public ownership of the means of production. That is, of course, if society is to escape the impending descent into barbarism.

Ted Reese is author of Socialism or Extinction: Climate, Automation and War in the Final Capitalist Breakdown